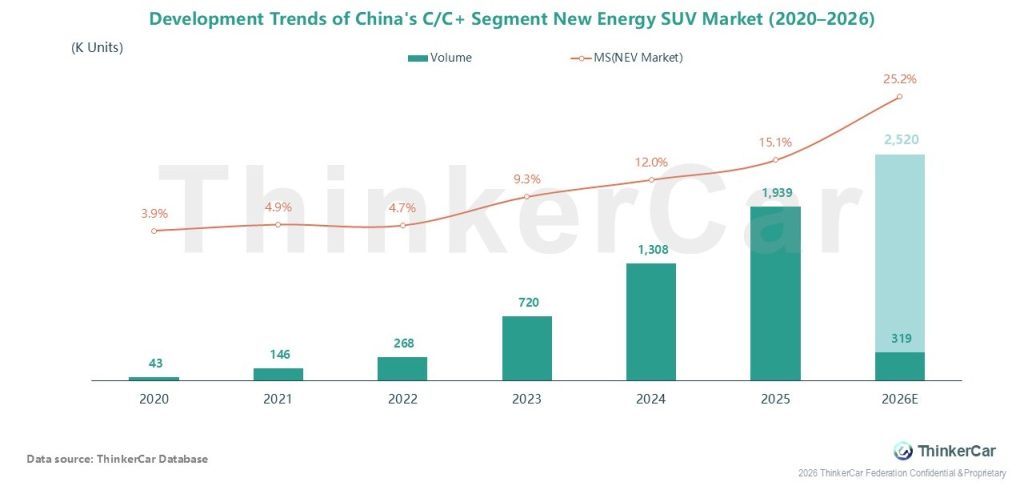

Between 2020 and 2025, China’s C/C+-segment new energy SUV market experienced explosive growth. Sales surged from 43k units to 1.94M units, and its share within the overall NEV market rose from 3.9% to 15.1%. In the first two months of 2026, sales reached 319k units. Full-year 2026 sales are projected to hit 2.52M units, with the market share increasing further to 25.2%. As a highly competitive segment for automakers, a large number of new models will enter the market in 2026

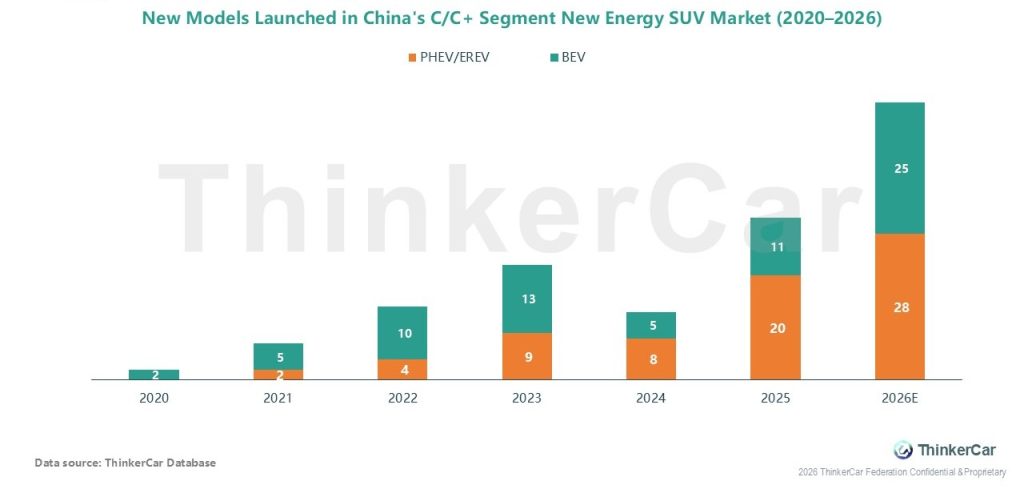

Over the same period, the number of new models launched in China’s C/C+-segment new energy SUV market grew steadily, rising from just 2 models in 2020 to 31 models in 2025. Looking ahead to 2026 (forecast), the pace of new model launches will accelerate significantly, with 53 new models expected to enter the market—including 28 PHEV/EREV models and 25 BEV models—reflecting intensified competition and strategic focus among automakers on this high-potential premium segment

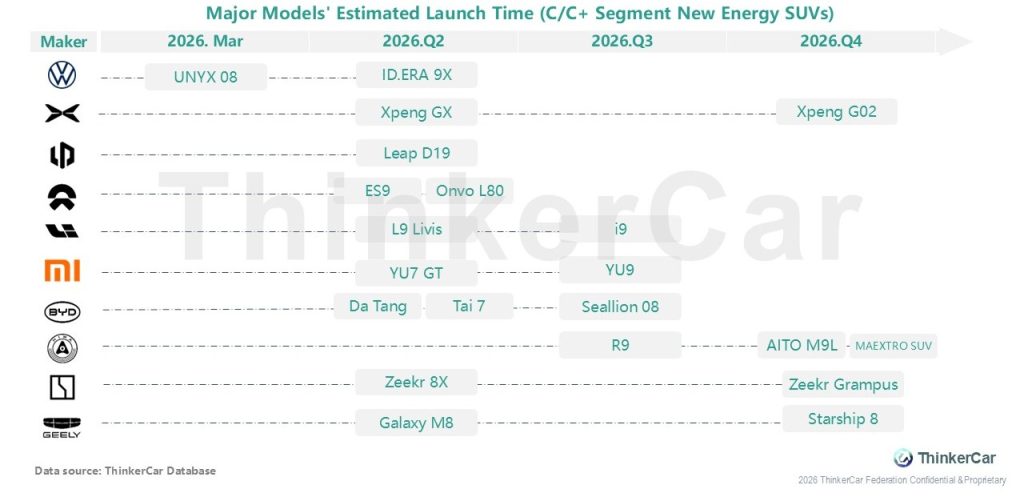

In terms of key product launches, models such as Xpeng GX, NIO ES9, Li L9 Livis, BYD Datang, and Volkswagen ID. ERA 9X are set to be released in Q2 2026, while Xiaomi Yu9, BYD Seal 08, and AITO M9L will launch in the second half of the year. This segment is poised for profound restructuring

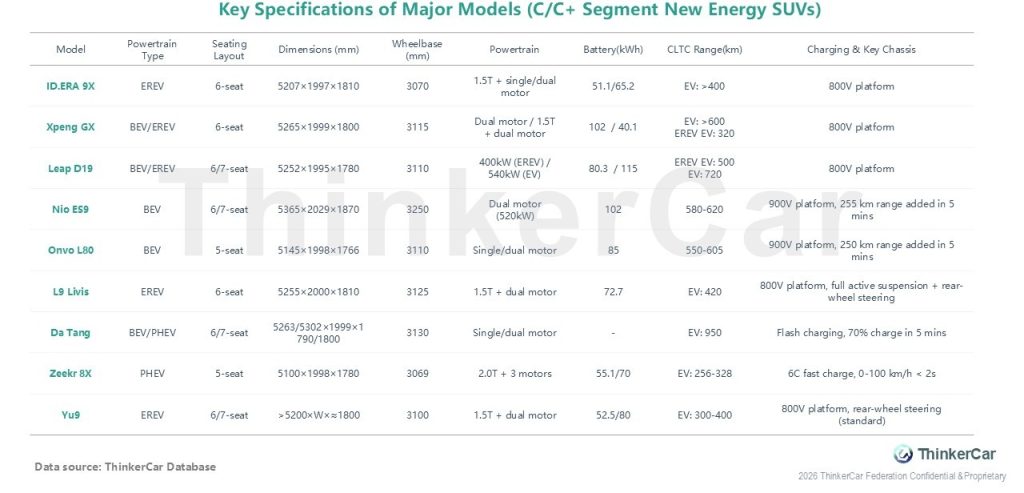

Based on key information, major models focus on powertrain, range, and intelligent configuration. Volkswagen ID. ERA 9X, Xpeng GX, and Leap D19 offer EV/EREV options with wheelbases over 3100mm, emphasizing space and range. NIO ES9 and Onvo L80 feature 900V fast charging, adding over 250km in 5 minutes. EREV/PHEV models like Li L9 Livis, BYD Da Tang, and Zeekr 8X deliver a combined range of over 1000km, driving further competition in the segment

ThinkerCar Data

chosen by over 200 renowned global enterprises