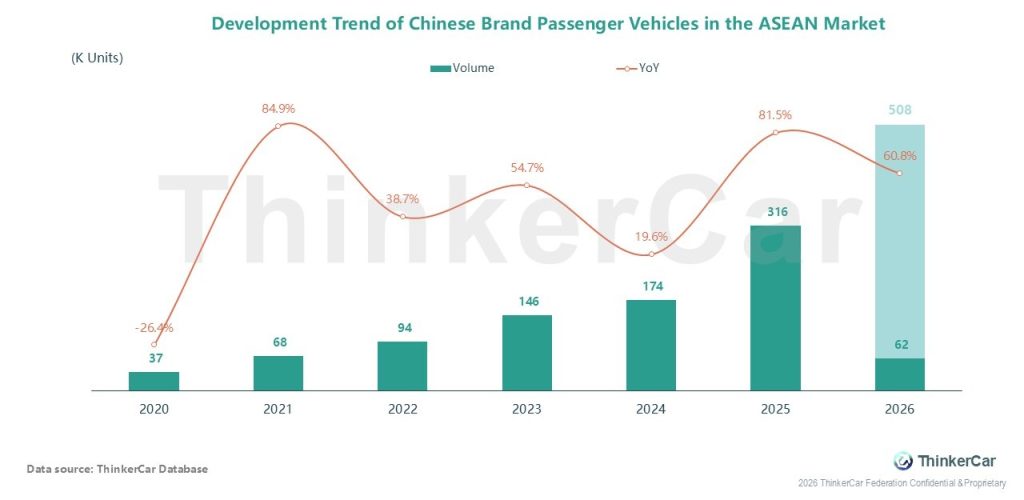

Following a 26.4% YoY decline in 2020 (37k units), Chinese brand passenger vehicles have demonstrated resilient and accelerating growth in the ASEAN market, rising from 68k units in 2021 to 316k units in 2025 with double-digit YoY growth throughout. A strong start of 62k units in January 2026 supports a projected full-year sales volume of 508k units (a 60.8% YoY increase), cementing the position of Chinese brands as a key growth driver in the region

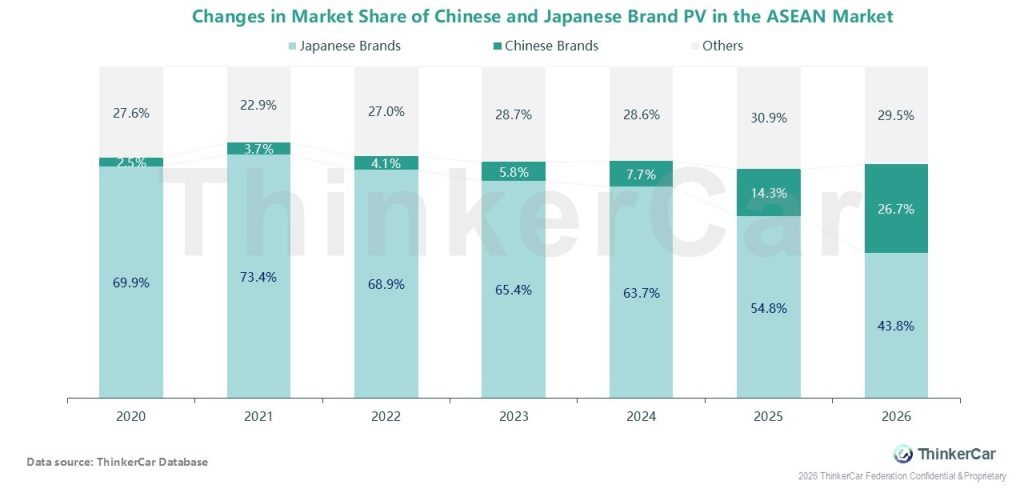

The competitive landscape of the ASEAN passenger vehicle market is undergoing a profound structural shift, as Chinese brands rapidly erode the long-standing dominance of Japanese brands. Between 2020 and 2025, the market share of Japanese brands plummeted from 69.9% to 54.8%, while that of Chinese brands surged from 2.5% to 14.3%. By 2026, Chinese brands are projected to further rise to 26.7%, with Japanese brands declining to 43.8%, marking a fundamental reshaping of the regional automotive competitive landscape

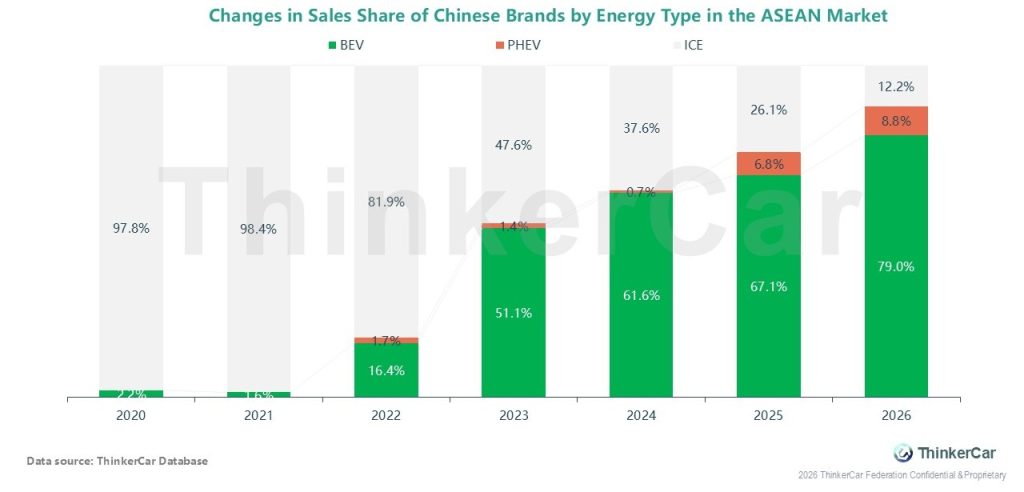

Chinese brands in the ASEAN market are undergoing a profound product transformation, shifting decisively from an ICE-dominated portfolio to a NEV-led one. In 2020, ICEs accounted for 97.8% of their sales, but this share plummeted to 12.2% by 2026. Conversely, BEVs have emerged as the dominant force, surging from a mere 2.2% in 2020 to a projected 79.0% in 2026. PHEVs have also grown steadily, reaching 8.8% in 2026. This transition underscores Chinese brands’ strategic focus on electrification, enabling them to leverage their technological advantages and drive the region’s automotive evolution

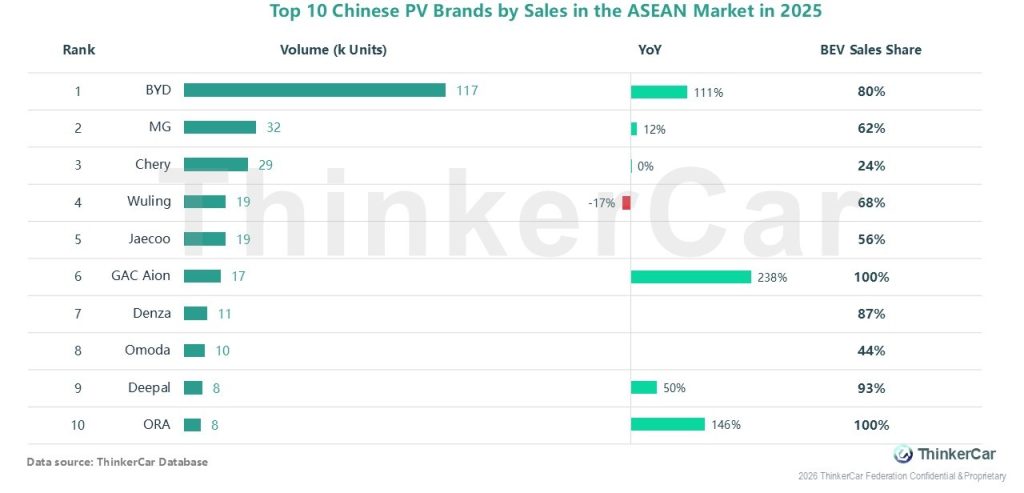

In 2025, BYD topped the top 10 Chinese PV brands in ASEAN with 117k units sold, a 111% YoY increase, and an 80% BEV share. MG and Chery followed with 32k and 29k units, while Wuling is the only top-10 brand to see a YoY decline (-17%). Notably, new energy-focused brands like GAC Aion, Deepal, and ORA achieved explosive growth, with BEV shares all exceeding 80% (GAC Aion and ORA at 100%), underscoring electrification as a core driver of Chinese brands’ rapid expansion in the region

BYD dominated as the top-selling Chinese passenger vehicle brand across all key ASEAN markets in 2025, leading in Thailand (41.1k), Malaysia (10.4k), Singapore (9.3k), the Philippines (9.4k), and Indonesia (46.8k). Chery and MG follow closely in several markets, while Wuling and Aion also rank among the top three in Indonesia and Thailand respectively, underscoring BYD’s dominant regional position

ThinkerCar Data

chosen by over 200 renowned global enterprises