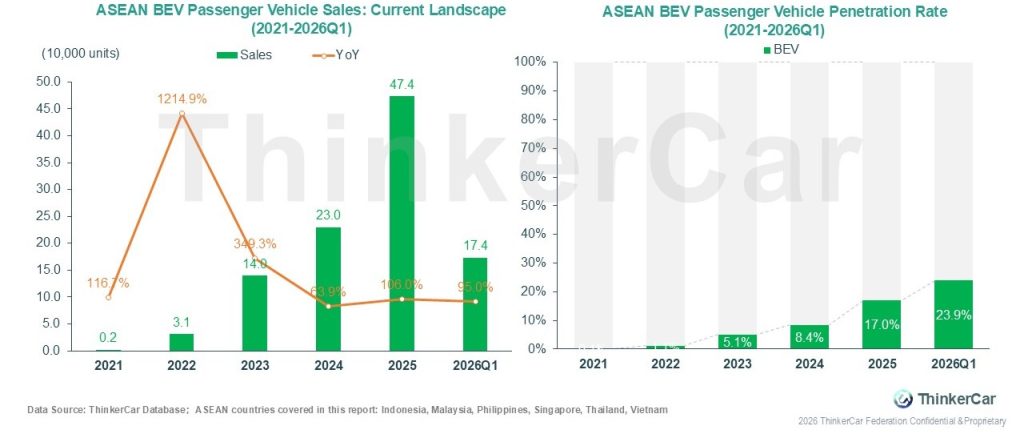

2021-2026 Q1, the ASEAN BEV passenger vehicle market continued along the region-wide trajectory of explosive NEV expansion, sustaining high-speed growth as the dominant sub-segment. Starting from a near-zero base, 2021 annual sales amounted to just 2,000 units. Sales then expanded at a steady pace, reaching 474,000 units in 2025. 2026 Q1 quarterly sales reached 174,000 units, with YoY growth holding at a robust 95%. As sales continued to scale, BEV penetration rose sharply in tandem, climbing from a minimal level in 2021. The penetration rate reached 17.0% in 2025 and further rose to 23.9% by Q1 2026, firmly establishing BEVs as the primary driver of the region’s electrification.

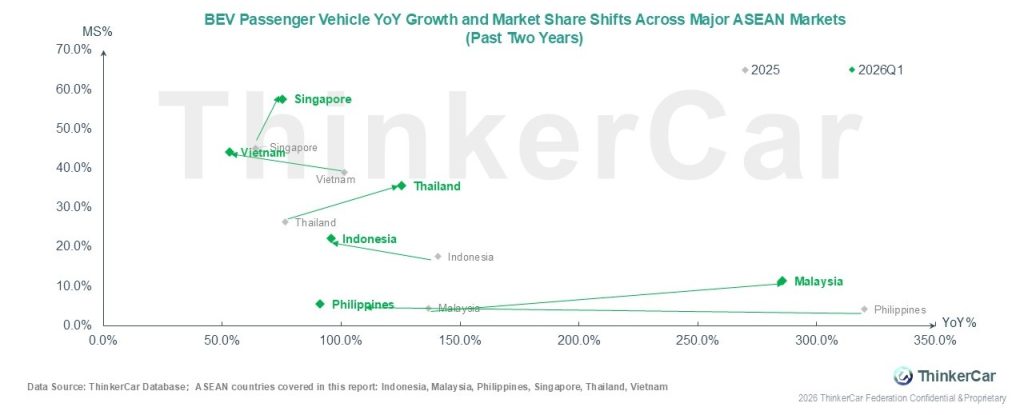

2025-2026 Q1, the ASEAN BEV passenger vehicle market displayed clear tiered differentiation, closely mirroring the rhythm of the broader regional NEV market. On penetration rate, Singapore leads the region, surging from approximately 46% in 2025 to nearly 60% in Q1 2026. Vietnam holds a strong second-tier position, maintaining an elevated market share. Thailand’s share and growth rate are both rising, closing in on the leading markets. Indonesia ranks in the second tier, with a high market share but a temporary moderation in growth. Among lower-tier markets, Malaysia leads the entire region with a YoY growth rate of nearly 300%, achieving a substantial jump in market share. The Philippines, though seeing slower growth off a high prior-year base, continued to record modest share gains.

As the ASEAN NEV passenger vehicle market expanded rapidly, its brand landscape evolved from early-stage fragmented multi-brand competition to a structure dominated by VinFast and Chinese brands. In the early phase of market development (2022), Chinese brand Wuling led with 8,000 units, while VinFast, BMW, MG and others held fragmented shares, with no brand exceeding 10,000 units annually. From 2023, VinFast rose to the top on the strength of its home-market advantage, with sales climbing from 35,000 units to 187,000 units in 2025, holding the regional top spot. Chinese brand BYD posted breakthrough growth, rising from 34,000 units in 2023 to 126,000 units in 2025, securing second place and forming a dominant two-player duopoly with VinFast. During the same period, MG, AION, Neta, Wuling, and other Chinese brands collectively scaled up, steadily eroding the market positions of incumbent international brands and Tesla. Chinese brands accounted for more than half of the top-ten ranking in 2025. In Q1 2026, the market saw the two-leader dynamic continue, with VinFast and BYD posting quarterly sales of 55,000 and 41,000 units respectively. Jaecco, Proton, Geely, and other brands rapidly moved up the rankings. Chinese brands as a whole maintained strong expansion momentum, emerging as the primary force driving NEV market growth across the region.

ThinkerCar Data

chosen by over 200 renowned global enterprises