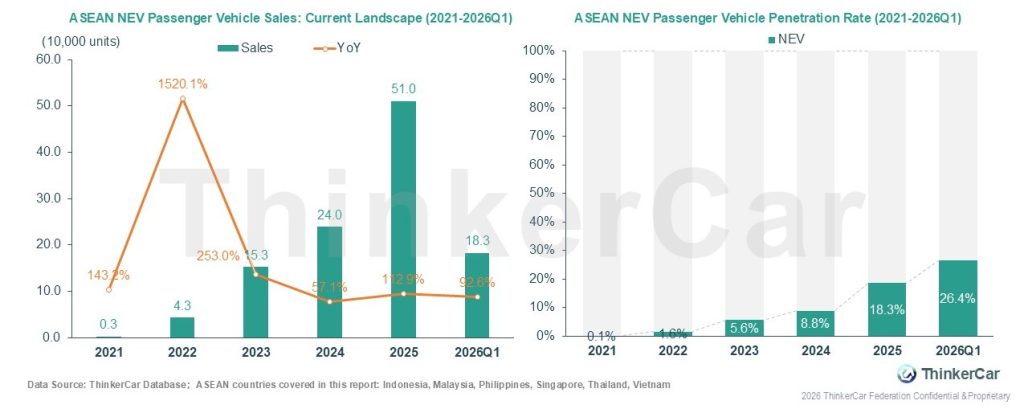

2021-2026 Q1, the ASEAN NEV passenger vehicle market was in a phase of explosive, high-velocity penetration from a near-zero base. 2021 annual sales stood at only 3,000 units. The market then entered a period of exponential growth; although the YoY growth rate gradually moderated, annual sales continued to roughly double each year. 2025 Sales climbed to 510,000 units, and in 2026 Q1 quarterly sales reached 183,000 units, with YoY growth holding at a strong 92.6%. As volume continued to expand, the NEV passenger vehicle market’s penetration rate rose sharply in tandem, climbing from a mere 0.1% year by year since 2021, and by 2026 Q1 has surpassed 26.4%. ICE vehicle market share has been steadily compressed, and the region’s electrification trajectory has entered an accelerated phase.

Over the past two years, NEV passenger vehicle penetration rates have risen across all major ASEAN markets, with growth momentum showing structural divergence. On the penetration rate dimension, Singapore leads, with a Q1 2026 penetration rate of 60%. Vietnam, Thailand, and Indonesia follow closely, at 44%, 38%, 23% respectively. Malaysia and the Philippines are achieving rapid penetration from a low base: Malaysia‘s penetration rate has risen from 4.5% to 11.3%, a particularly notable gain. On the growth rate dimension, Malaysia leads with a YoY increase of 285.7% ; Thailand and Singapore maintain steady growth, while Vietnam, Indonesia, and the Philippines have seen a temporary moderation in growth rates. Overall, the market is taking shape as one where “leading high-penetration markets consolidate their positions while late-mover, low-base markets accelerate their expansion”.

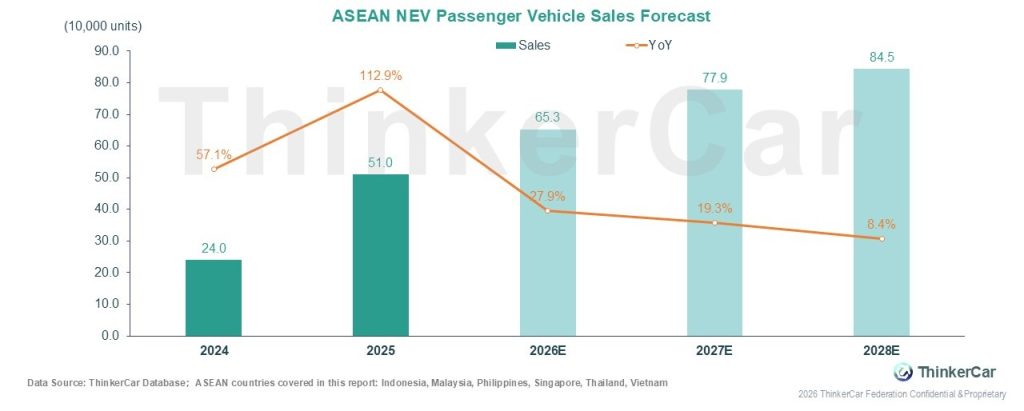

Supported by the rollout of the ASEAN Energy Efficient Vehicle (EEV) regional tariff harmonization framework and the continued release of consumer-side incentive policies across member states, in 2026 the ASEAN NEV passenger vehicle market is set to sustain steady growth, with full-year sales projected at 653,000 units, representing a YoY growth rate of 27.9%. The primary growth drivers at this stage are the concentrated release of regional manufacturing capacity, the accelerating expansion of Chinese automakers, and ongoing improvements to charging infrastructure. Looking ahead to 2027–2028, as the market base expands and consumer subsidies are progressively phased out across member states, growth is expected to slow steadily, with 2028 full-year sales projected at 845,000 units, reflecting YoY growth of 8.4%. By then, the market will have formally entered a stage of large-scale, mature development.

In terms of regional structure, Vietnam is set to continue leading the ASEAN market, with a 2028 volume share of 31.4%; Thailand holds second place on the strength of its industrial chain and export advantages, with a share of 25.1%; Indonesia‘s market is expanding rapidly, with share rising to 22.9%; Vietnam, Thailand, and Indonesia combined will account for over 80%; Malaysia, the Philippines, and Singapore collectively account for approximately 19%, with the regional structure exhibiting a stable configuration of “Vietnam-Thailand Dominance, Multi-Point Support”

ThinkerCar Data

chosen by over 200 renowned global enterprises